Daily Market Wrap

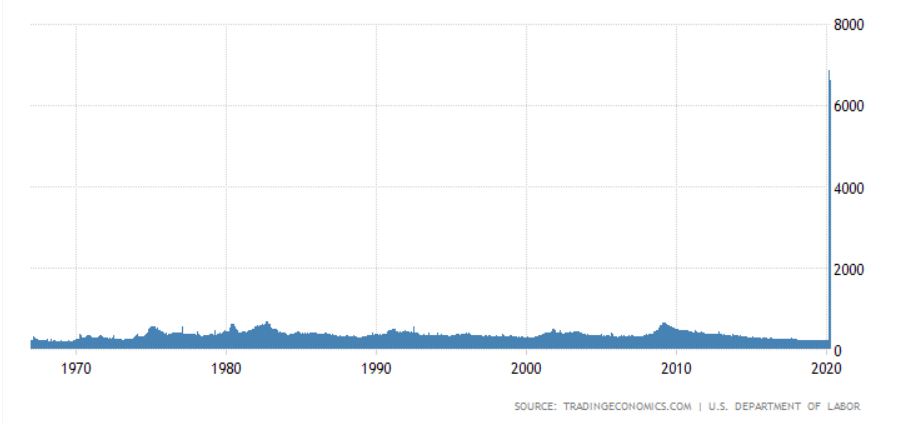

Economic data continued to reveal the extensive damage caused by the coronavirus, specifically a 7.5% plunge in personal spending for March and a larger-than-expected 3.839 million initial jobless claims, coming in about 300,000 more than predicted, and pushing the six-week total above 30 million. That implies a jobless rate of around 22%, the worst since the Great Depression, and more than twice the 10% peak reached in 2009.

Initial Claims

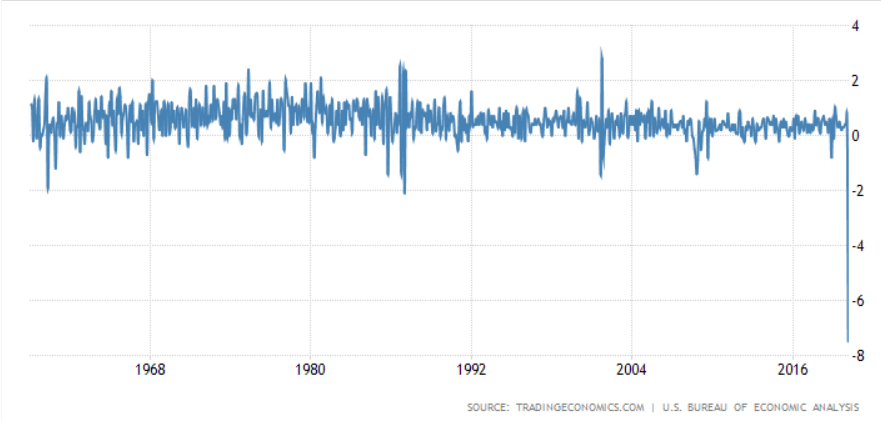

Personal income declined 2.0% m/m in March (consensus -1.5%) while personal spending plunged 7.5% (consensus -3.6%). The PCE Price Index dropped 0.3% and the core PCE Price Index, which excludes food and energy, declined 0.1%. The report is a precursor to what will be much worse data for April, which will drive a much worse decline in GDP than the 4.8% annualized decline registered in the first quarter.

Personal Spending

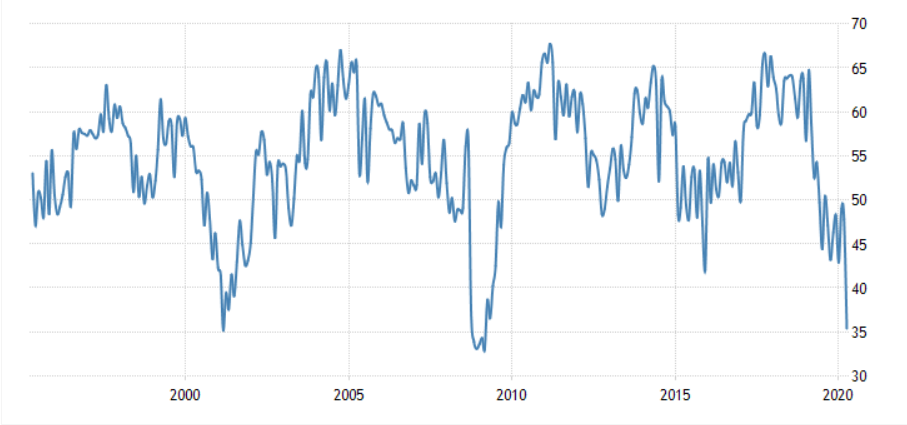

Chicago PMI for April declined to 35.4 (consensus 39.2) from 47.8 in March.

Chicago PMI

However, Central banks remained committed to supporting the financial system. The Fed expanded the scope and eligibility for its Main Street Lending Program, and the ECB said it will conduct net asset purchases under its EUR750 billion pandemic emergency purchase program through at least the end of the year.

Averages

After 3 days of leadership, small caps were a notable laggard due weakness in cyclicals and Regional Banks.. Strong results from Microsoft Corp., Facebook Inc. and Tesla Inc. limited losses in the tech-heavy Nasdaq, as well as the broader market. The major averages closed off the low of the day, except small cap Russell 2000 declined into the close.

S&P 500 ⇩ -1.00 %

NASDAQ ⇧ 0.20 %

DOW JONES ⇩ -1.17 %

RUSSELL 2000 ⇩ -3.68 %

SP-500 (daily) w/ 50 and 200-day simple moving averages. There are two areas I’m focused on, one is the 200-day moving average (blue) above around $3006

And…

SP-500 (3m) the $2860 area below which is the top of a 2+ week range.

The very clear 2 week range sets up the possibility of a failed breakout and bull trap. The 3C negative divergence into the breakout rally makes it a higher probability.

SPY (3m)

S&P sectors

Sector performance was a reversal of the week’s theme in that every sector was down, and the growth-sensitive cyclicals that have been the source of leadership, were the laggards. The mega-cap heavy Technology, Communications and Consumer Discretionary sectors outperformed ahead of Apple and Amazon earnings. Semiconductors (-3.7%) were an area of weakness within the technology space.

Materials ⇩ -2.97 %

Energy ⇩ -2.21 %

Financials ⇩ -2.52 %

Industrial ⇩ -1.98 %

Technology ⇩ -0.45 %

Consumer Staples ⇩ -1.19 %

Utilities ⇩ -2.30 %

Health Care ⇩ -0.46 %

Consumer Discretionary ⇩ -0.62 %

Real Estate ⇩ -0.70 %

Communications ⇩ -0.44 %

After negative 3C divergences in Financials Wednesday, Regional Banks (-4%) were one of the worst performing groups, weighing on Small Caps.

Regional Banks (30m) showed a negative divergence yesterday into the top of the channel, prices backed off today.

Regional Banks (30m) showed a negative divergence yesterday into the top of the channel, prices backed off today.

Industrials (30m) and Dow Transports closed just below support and back in the range.

Industrials (30m) and Dow Transports closed just below support and back in the range.

The $8400 area for Dow Transports is clearly a key technical/psychological level.

Dow Transports (5m)

Internals

Internals were as expected with NYSE Decliners (2066) outpacing Advancers (807) by a 2-1 ratio, and on heavy month-end volume of 1.5 bln. shares.

There is no Dominant price/volume relationship, and no 1-day oversold condition.

Treasuries

U.S. Treasuries ended the session near their flat lines, but were volatile intraday. The 2-year yield and the 10-year yield declined one basis point each to 0.18% and 0.62%, respectively.

The Washington Post ran an article that the White House is considering retaliatory actions against China over the handling of the corona-virus.

“Some administration officials have also discussed having the United States cancel part of its debt obligations to China”

While White House economic advisor, Larry Kudlow, denied the debt cancellation aspect of the story, treasuries were weak the rest of the day.

If you held someone’s debt and they said the would cancel it in retaliation, what would you do? I’d probably sell it while I could. Keep in mind that yields on the long end jumped Wednesday too as the Fed slowed the pace of bond purchases.

Currencies and Commodities

The U.S. Dollar Index declined -0.6% to 99.01.

There was some notable movement in currencies today.

AUD/USD (15m) the Aussie revealed a change in risk sentiment before the cash open in having broken the week’s up-trend.

AUD/USD (15m) the Aussie revealed a change in risk sentiment before the cash open in having broken the week’s up-trend.

Crude and bond yields have sent ugly macro market signals over the last few weeks, but currencies have stayed either positive or neutral at worst.

AUD/USD (15m)- this is the up-trend off the March low coming in tonight around 0.6460, that’s the level I think is important as it relates to the outlook from the FX market.

While on currencies, the Chinese yuan reacted negatively to the Washington Post story. I haven’t posted many charts of the yuan recently, as it has been quietly consolidating, but with this new potential flash-point between the U.S. and China, I have a feeling it’s going to be active.

USD/CNH (15m) the Chinese yuan sold off, or sent a risk-off signal and stocks traded down to new session lows.

USD/CNH (15m) the Chinese yuan sold off, or sent a risk-off signal and stocks traded down to new session lows.

The yuan was one of the currencies sending a risk-off warning in February with commodities and bond yields.

USD/CNH (daily) the first red arrow was a risk-ff signal over the corona-virus outbreak in Wuhan, the second was risk-off as the market crashed. The big bull flag consolidation (green) is risk-supportive, the period stocks have rallied. It’s almost the mirror opposite of the trend in Regional Banks and small caps. While the price consolidation is a big bull flag, a breakout from the flag would be bearish for risk assets.

Crude rose for a second day on signs fuel consumption is starting to recover in the world’s biggest economies.

WTI crude gained +22.8% to $18.58/bbl., but unlike yesterday’s double-digit rally, today was technically significant.

WTI Crude (60m) made a slightly higher high or cleared resistance on a closing rally above $18.26

Even with the 2-day rally, Crude’s price action over the last month is horrendous and a very ugly signal.

S&P futures (daily and WTI Crude (purple)

Gold futures lost -1.1% to $1,694.20/oz, still up some 6% in April. Today is the fifth day gold has been sold before the U.S. open.

GLD (15m) the price consolidation taking shape looks constructive and gold’s volatility continues to subside. GLD is pulling back closer to the $157 area I highlighted as an area of interest on the long side.

Summary

With Apple and Amazon earnings as the market’s focus, a flair up in U.S. -China tensions may have flown under the radar. The story that senior U.S. officials were considering retaliatory steps against Beijing for its handling of the pandemic was floating around Wednesday, but didn’t get any reaction from the market.

Stocks reacted by moving down to session lows. Bonds appear to have reacted by selling off, but what was notable to me today was the move in currencies being they have been the one solid risk-supportive signal for the last month.With everything going on it can be easy to forget there are still tariffs in place and there’s still a trade war, albeit at a truce due to the phase I deal. It sounds like that truce may unravel.

Overnight

In afterhours earnings, Visa’s CEO warned the firm will be challenged “for a number of quarters” even as declines in spending on its network began to moderate in April. Amazon reported $75.5 billion in sales in the quarter, but said it’ll book $4 billion in costs related to the virus, which weighed on shares. And Apple’s quarterly revenue grew 1%, driven by strong sales of digital services and wearable devices. It didn’t issue a forecast for the first time in more than a decade. However, CEO Tim Cook said the company saw a “pickup” in the second half of this month, after a “very depressed” period in late March and early April. Apple also increased its share buyback plan by $50 billion.

S&P futures are down -1.1%

S&P futures (1m) drop further from the afternoon consolidation.

WTI crude is up +3% and holding above the $18 area, however, copper has fallen further.

Currencies look a little more risk-off with the Aussie and Chinese Yuan falling further against the dollar into the overnight session.

USD/CNH (1m)

USD/CNH (1m)

AUD/USD (1m)

AUD/USD (1m)

Tomorrow investors receive the ISM Manufacturing Index for April, Construction Spending for March, and auto and truck sales for April on Friday.