Daily Wrap – March 10, 2020

The stock market rebounded about 5%, while Treasuries pulled back sharply in Tuesday’s volatile session as investors weighed the possibility of a fiscal stimulus package. The major indices started the session up nearly 4%, then briefly dipped negative led by Small Caps, and later staged a strong rally into the close.

President Trump said last night he wanted payroll tax cuts and support for hourly workers to help mitigate the impact and spread of the coronavirus. Mr. Trump added today that he also wants to protect airlines, cruise ships, and shipping industries. On top of that, he pitched the idea of a 0% payroll tax rate for the rest of the year. Republican Senate Leader McConnell (R-KY) reportedly said he didn’t like the idea of a payroll tax cut, but Treasury Secretary Mnuchin said he thinks there’s bipartisan interest in getting something done.

Airline stocks were among the biggest beneficiaries from President Trump’s comments. Delta Air Lines (DAL +4.5%), American Airlines (AAL +15.3%), and United Airlines (UAL +12.4%) announced capacity cuts due to weakened travel demand, but shares rallied on the potential for government aid.

Averages

NASDAQ 100 outperformed slightly. Small Caps under-performed and IWM traded down to the $128 target from Sunday night with an intraday low of $128.02.

S&P 500 ⇧ 4.92 %

NASDAQ ⇧ 5.34 %

DOW JONES ⇧ 4.89 %

RUSSELL 2000 ⇧ 2.85 %

SP-500 (daily) finding support at the May/June low reached yesterday. The close was strong at the day’s high

SP-500 (daily) finding support at the May/June low reached yesterday. The close was strong at the day’s high

NASDAQ 100 (daily) closed back above its 200-day ($8178.51)

NASDAQ 100 (daily) closed back above its 200-day ($8178.51)

S&P and Dow saw some resistance at Feb. 28th’s low, but managed to close just above.

SP-500 (5m)

SP-500 (5m)

Dow (5m)

Due to the NASDAQ 100’s out performance, it was the first of the major averages to reveal a bearish flag. The Dow and S&P’s resistance kept them from the upward sloping flag until late in the session.

NASDAQ 100 (5m)

NASDAQ 100 (5m)

Dow Transports also reveal a bear flag correction/consolidation![]() Dow Transports (15m)

Dow Transports (15m)

As we saw last week, early flags can expand.

S&P sectors

All 11 sectors closed higher in a broad-based oversold relief rally, although volatile. As an example, the Energy sector traded as high as +8.5% on the open, lost more than -1.6%, then closed up +4.75%. The sectors most beaten up recently were among the best performers including Financials and Banks.

The defensive sectors that held up best on the sell-off yesterday, were today’s laggards amid the risk-on tone and higher yields.

Materials ⇧ 4.06 %

Energy ⇧ 4.74 %

Financials ⇧ 5.87 %

Industrial ⇧ 5.18 %

Technology ⇧ 6.67 %

Consumer Staples ⇧ 2.87 %

Utilities ⇧ 0.93 %

Health Care ⇧ 3.43 %

Consumer Discretionary ⇧ 5.53 %

Real Estate ⇧ 4.86 %

Communications ⇧ 5.10 %

The Energy sector’s near 5% advance is a drop in the bucket relative to its losses.

Energy (15m) today at the green trend line, the line above was my downside target before the OPEC led decline in crude yesterday.

Energy (15m) today at the green trend line, the line above was my downside target before the OPEC led decline in crude yesterday.

Financial sector (15m) is another that reached the downside target and is bouncing from it.

Financial sector (15m) is another that reached the downside target and is bouncing from it.

Most other sectors, with targets covered in last night’s Daily Wrap, have not hit their second leg downside targets yet.

Industrial sector (15m) another early example of a bear flag thus far.

Industrial sector (15m) another early example of a bear flag thus far.

And a few more…

Technology sector (15m)

Technology sector (15m)

Health Care (15m) bearish flag- note it’s a defensively oriented sector and like the others, did not trade below last week’s low yesterday.

Health Care (15m) bearish flag- note it’s a defensively oriented sector and like the others, did not trade below last week’s low yesterday.

Consumer Discretionary (15m)

Consumer Discretionary (15m)

Communications sector (15m)

Communications sector (15m)

Internals

Advancers (2167) are 3:1 over Decliners (668) on Volume of 1.8 bln. shares.

The Dominant price/volume relationship is Close Up/Volume Down, the most bearish relationship that’s typical of an oversold correction.

Treasuries

The 2-year yield finished 15 basis points higher at 0.47%, and the 10-year yield finished 25 basis points higher at 0.75%. These are big moves for a day, but in the context of the decline, pretty normal. Yields did lead the S&P higher earlier today as seen in this post...

From the post linked above.

I mentioned using TLT’s expected pull back as an indication of where we might expect to see yields end their correction.

TLT (15m) the area is $157-$160.

Currencies and Commodities

The U.S. Dollar Index rose 1.6% to 96.45.

In addition to TLT’s $157-$160 area…

USD/JPY (30m) is also correcting, in fact it started yesterday even before stocks. The red trend line above has been strong resistance for 3 weeks and stocks have turned down as the pair reached this area.

USD/JPY (30m) is also correcting, in fact it started yesterday even before stocks. The red trend line above has been strong resistance for 3 weeks and stocks have turned down as the pair reached this area.

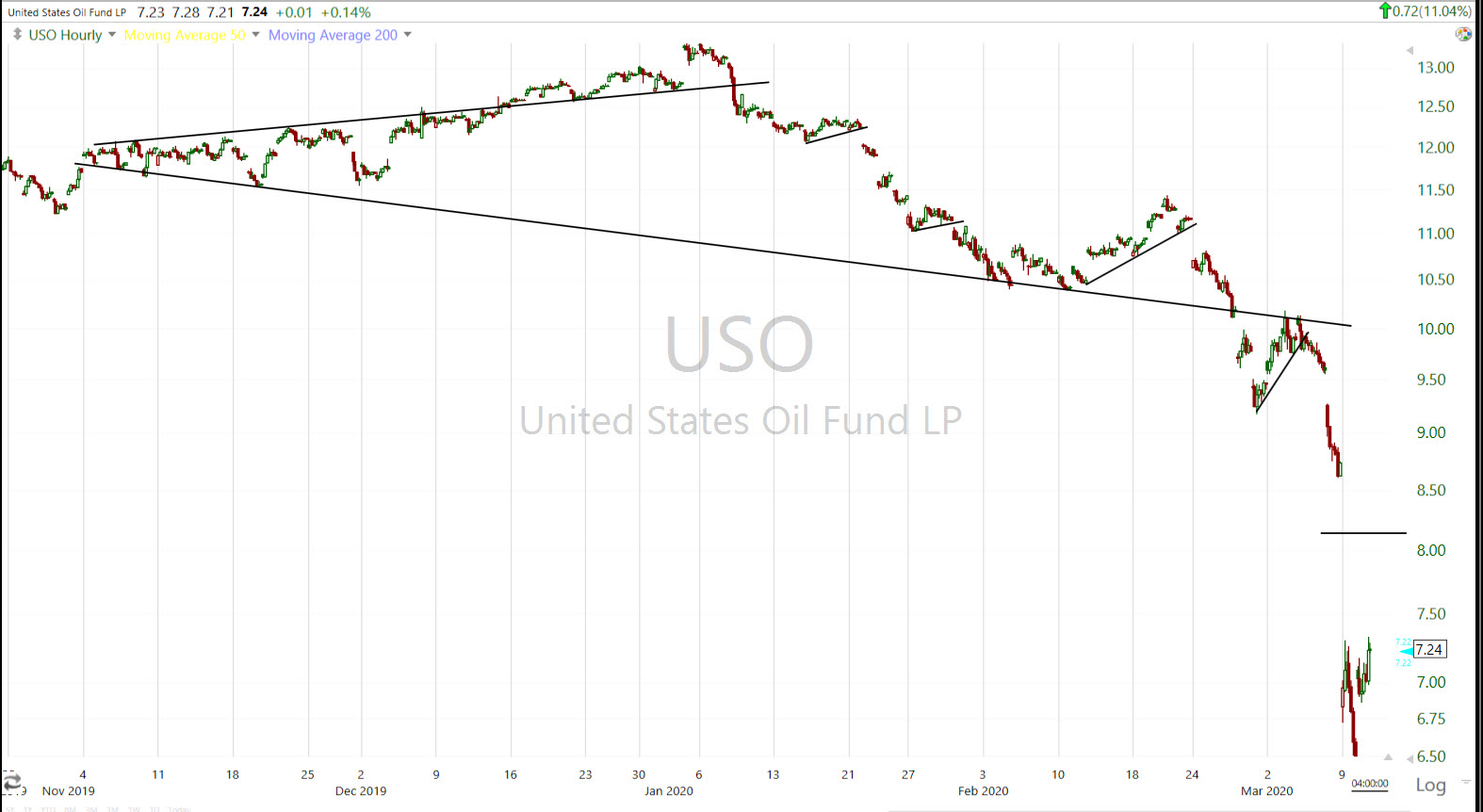

Oil rebounded from its worst day since 1991 after reports indicated that Russia could be interested in discussions to stabilize oil markets. WTI crude gained +10.2% to $34.25/bbl. , however it too was a drop in the bucket.

USO (60m)

Summary

Although very volatile, today’s price action is thus far a bearish consolidation. Internals reflect the same. I expect it can continue a bit longer as Treasuries potentially meet a short term pull back target. Also keep an eye on USD/JPY which I mentioned before the open today.

I may change some of the price targets from Sunday given there’s more information, but the targets are not substantially different. The revised targets will depend on how long the consolidation goes on and if it maintains the same trend. Right now they are about 1% lower than Sunday night’s targets, so not substantially different and if the consolidation/bounce carries on for another day or so, they may be exactly the same.

There are a lot of moving parts to keep an eye on, but small caps’ relative performance is one aspect that has been very helpful. I’ll assess risk and act as opportunities arise, but I would prefer the deep oversold conditions work off and the S&P trades at least up to or above $3000 before entering new short trades.

Overnight

S&P futures are down -1.1% after the 5:30 White House press briefing offered few details on President Trump’s stimulus plan. This should be quite a political fight being he and House leader Nancy Pelosi don’t have a good relationship, and in an election year. There’s some local resistance in the area at 2880.

Investors will receive the Consumer Price Index for February, the Treasury Budget for February, and the weekly MBA Mortgage Applications Index on Wednesday.