Stock Market Analysis -Bull Flag’s Breakout

Although the ride has been bumpy, I’m pretty happy with last Friday’s Afternoon Update forecast for this week,

“I do like the looks of the charts heading into next week to add to the relief rally’s rebound. There may be a brief consolidation fairly early in the week, but that’s a positive in my view and can help dial in targets and timing more accurately. My plan is the same as it has been. I do have a small long S&P position via UPRO, but the more appealing trade is to sell/short-sell into a strong rebound and I think that happens before the mid-March FOMC.”

However long it lasts, the market seemed a little overdone on the fear side and took today’s headlines as a little bit of relief, opening the door for the averages to breakout of bull flags. In last night’s Daily Wrap (summary and overnight sections) a few things were evident. One was Fear was moving to an extreme and extremes are often contrarian – whether volatility’s term structure in backwardation 4 of 5 days, or the Fear and Greed Index reaching extreme fear, the bearish sentiment seemed overdone.

Secondly, we got the first glimpse of the safe-haven (and potentially technical issues related to Russian sanctions and treasury short squeezes) fading…

“Treasury futures have pulled back off intraday highs. The 2-year yield is no up 9 basis points and the 10-year yield is up 5 basis points. This could be the start of some unwinding of safe-havens (potential inside information out there with regard to Russia/Ukraine). It’s something of interest to be aware of tonight.”

I have to say just looking at Monday/Tuesday’s price percentage losses, it would be easy to overlook the overall bullish consolidation bias, which is why I’ve focussed less on the day-to-day or intraday craziness, and more on the emerging price trend of consolidation developing as expected in the earlier part of the week like the bull flags.

Stocks rallied past another spike in oil prices amid hope surrounding the Russia-Ukraine conflict and a potentially less-hawkish Fed. It wasn’t just positive-sounding Russia/Ukraine headlines, but within a very mixed bag of comments from Powell in his testimony on Capitol hill, the one that held some resonance was that Powell affirmed a single rate-hike in March, but opened the door for a 50 bps hike in the future. No doubt this more moderate initial rate hike has everything to do with the geopolitical situation. I’m reminded of the song, “Them Bones”…

“toe bone is connected to the foot bone, the foot bone is connected to the ankle bone, the ankle bone is connected to the shin bone”

Here are a few soundbites from Powell’s first say of the 2-day semiannual testimony before Congress…

The Fed’s Bullard said that the current inflation environment does compare to the 1970’s. Echoing Bullard’s hawkish sentiment, the Fed’s Evans says that Fed policy is “wrong-footed” and needs an upward adjustment.

On a related note, the Fed’s Beige Book noted that economic activity expanded at a modest to moderate pace between mid-January and February 18. Some Districts reported a temporary weakening in demand in the hospitality sector due to increased COVID-19 cases.

On the economic front we saw better-than-expected ADP Employment Change report ahead of Friday’s important Payrolls report. ADP estimated 475,000 additions to private sector payrolls in February (consensus 350,000)

Averages

Small Caps and Dow Transports (+2.6%) had been pointing to improving risk sentiment yesterday and both followed through with better relative performance today, which bodes well for follow-through on today’s breakout from bull flag consolidations.

S&P-500 ⇧ 1.85 %

NASDAQ ⇧ 1.70 %

DOW JONES ⇧ 1.79 %

RUSSELL 2000 ⇧ 2.51 %

All of the major averages broke out of the week’s bull flags. S&P and Small Caps looked better on the breakout as they overcame the week’s highs.

SP-500 (5m)

SP-500 (5m)

While the Dow and NASDAQ-100 also broke out of bull flags, their breakouts were less definitive as they were unable to push through the week’s highs or local resistance.

NASDAQ-100 (5m)

NASDAQ-100 (5m)

Still, the fact that Small Caps and Transports outperformed sends a bullish message. Transports even managed to overcome the 200-day sma.

Dow Transports (daily)

Dow Transports (daily)

There wasn’t as much improvement on 3C charts as I would have expected to see, but for the most part they’re not in bad position either with QQQ, followed by IWM (5m) looking the best.

In trying to keep short term price action in context of the bigger picture, NASDAQ experienced its first Death Cross (50-day crossing below the 200-day) since April 2020, and that suggests that 2022 is not going to be an easy year for equities.

NASDAQ-100 (daily)

NASDAQ-100 (daily)

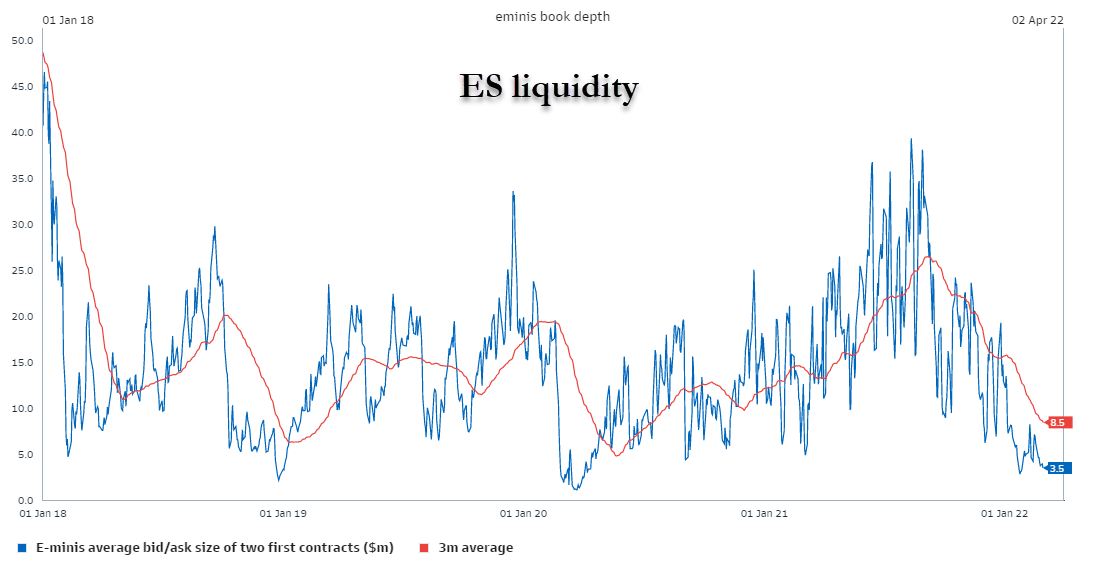

While Powell dismissed concerns about liquidity in the plumbing of the global financial system, it is clear there are emerging issues. Equity index liquidity is near record lows and that tends to exacerbate price swings (both up and down). That’s worth considering when entering and managing positions so you’re not whipsawed in and out of trades. In this kind of environment I generally reduce position size so I can widen stops, and pay less attention to intraday swings, or even day to day swings, and focus on broader trends (i.e. the week’s bull flags which were a bullish signal amid -1.8% benchmark losses in the first 2 days of the week). The context offered by multiple timeframe analysis matters.

VIX fell -7.75% today. VIX still displays relative strength on the week. The Absolute breadth index traded into the 22’s today so it still hasn’t triggered a sub-14 print.

After being in backwardation 4 of the last 5 days and starting there this morning, volatility’s term structure came out of backwardation today.

SP-500 (daily) and term structure. This is a modestly bullish signal of a short term low (extreme of fear and extremes are often contrarian signals).

SP-500 (daily) and term structure. This is a modestly bullish signal of a short term low (extreme of fear and extremes are often contrarian signals).

This afternoon VXX’s 3C charts reflected what I think is some nervousness ahead of tomorrow’s Russia/Ukraine talks, and who can blame investors as fluid as the situation and headlines have been.

VXX (1m) this isn’t the kind of signal that suggests someone knows something, it’s along the lines of the normal nervousness and hedging today’s gains in front of the latest round of talks tomorrow.

VXX (1m) this isn’t the kind of signal that suggests someone knows something, it’s along the lines of the normal nervousness and hedging today’s gains in front of the latest round of talks tomorrow.

S&P sectors

All 11 S&P 500 sectors closed higher, and 29 of the 30 Dow components closed higher. The cyclical Financials, Energy, Materials and Industrials sectors each rose more than 2.0%, as did Technology sector. The Communications sector underperformed on a relative basis.

Materials ⇧ 2.20 %

Energy ⇧ 2.29 %

Financials ⇧ 2.59 %

Industrial ⇧ 2.13 %

Technology ⇧ 2.17 %

Consumer Staples ⇧ 1.07 %

Utilities ⇧ 1.22 %

Health Care ⇧ 1.51 %

Consumer Discretionary ⇧ 2.10 %

Real Estate ⇧ 1.78 %

Communications ⇧ 0.86 %

Despite the sharp rise in yields, Growth style factors (Russell 1000 Growth) held up well today (+1.65%), but as is often the case, Value (Russell 1000 Value +2%) held up better amid higher yields.

Semis (SOX +3.4%) outperformed, as did Banks (KBW Index +3.6% and Regional Banks +4.45%), which was not the case yesterday and points to a more bullish environment as each of the groups has a tendency to lead their respective sectors, just as Transports tend to lead the Dow and Small Caps tend to lead the broader market.

Internals

NYSE Advancers (2286) outpaced Decliners (897) by more than a 2-to-1 margin on lighter Volume of 1.1 bln. shares. NASDAQ advancers (2714) fell short of a 2-to-1 margin over Decliners (1525) likely as a result of relative pressure on growth stocks due to a rapid rise in yields. Still, advance/decline lines are either neutral or constructive.

The Dominant price/volume relationship (except the Dow) was Close Up/Volume Down, which taken with internals and all 11 sectors green, results in a 1-day overbought condition. On that note breadth oscillators have reset, as they usually do coming out of oversold lows, to overbought, reaching 93 intraday and settling at 87.

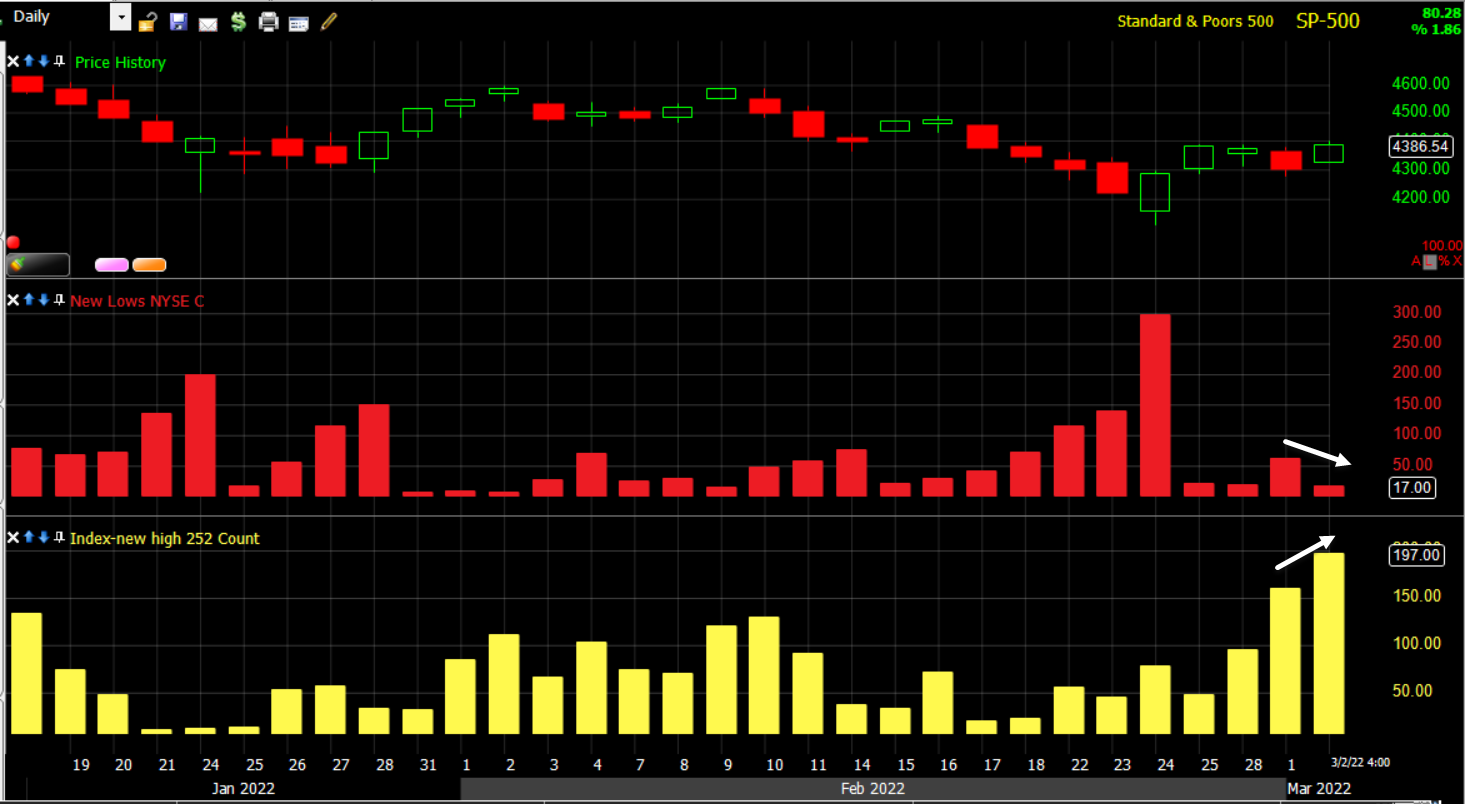

NYSE new 52 week lows dipped as they should and NYSE new highs rose for a 3rd day. Internals and participation look much better than the averages’ price performance on Monday/Tuesday might suggest and that’s saying something as internals have steadily and notably deteriorated for a year.

NYSE new 52 week lows dipped as they should and NYSE new highs rose for a 3rd day. Internals and participation look much better than the averages’ price performance on Monday/Tuesday might suggest and that’s saying something as internals have steadily and notably deteriorated for a year.

Treasuries

Treasury yields rose double-digit basis points after a two-day plunge, illustrating how negative sentiment had gotten because of the geopolitical tensions. The 2-year yield jumped 22 basis points to 1.52%, and the 10-year yield jumped 16 basis points to 1.87%. As massive as the jump in yields was today, it has to be kept in context of recent bond market volatility.

10-year yield’s (15m) rebound today (green) retraced yesterday’s flight to safety plunge and then a little, but not the plunge from Friday. So far I view this as a correction, but if yields see a rapid, sharpo move higher continue, that’s going to pressure equity valuations as we have seen so many times in the past year.

10-year yield’s (15m) rebound today (green) retraced yesterday’s flight to safety plunge and then a little, but not the plunge from Friday. So far I view this as a correction, but if yields see a rapid, sharpo move higher continue, that’s going to pressure equity valuations as we have seen so many times in the past year.

Powell and other Fed officials’ comments restored some of the focus on the Fed and while Ukraine figures into the Fed’s thinking, perhaps the market got a little carried away with thinking it would have more impact on the Fed. As a result, the yield curve retraced much of yesterday’s steepening…

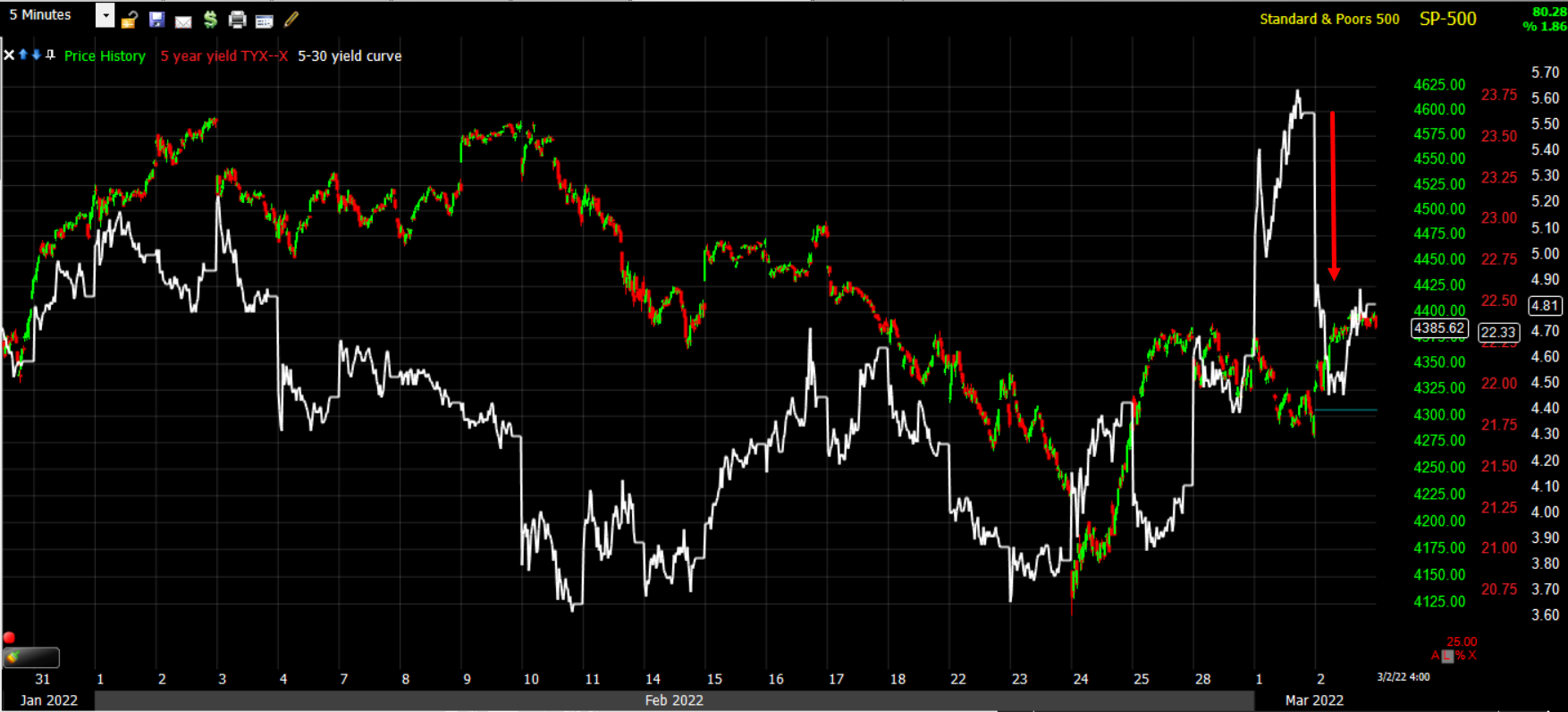

SP-500 (5m0 and 5s-30s yield curve. These are overreactions and corrections of overreactions, but in the near term I view this as fairly constructive for the market’s breakout from bull flags.

SP-500 (5m0 and 5s-30s yield curve. These are overreactions and corrections of overreactions, but in the near term I view this as fairly constructive for the market’s breakout from bull flags.

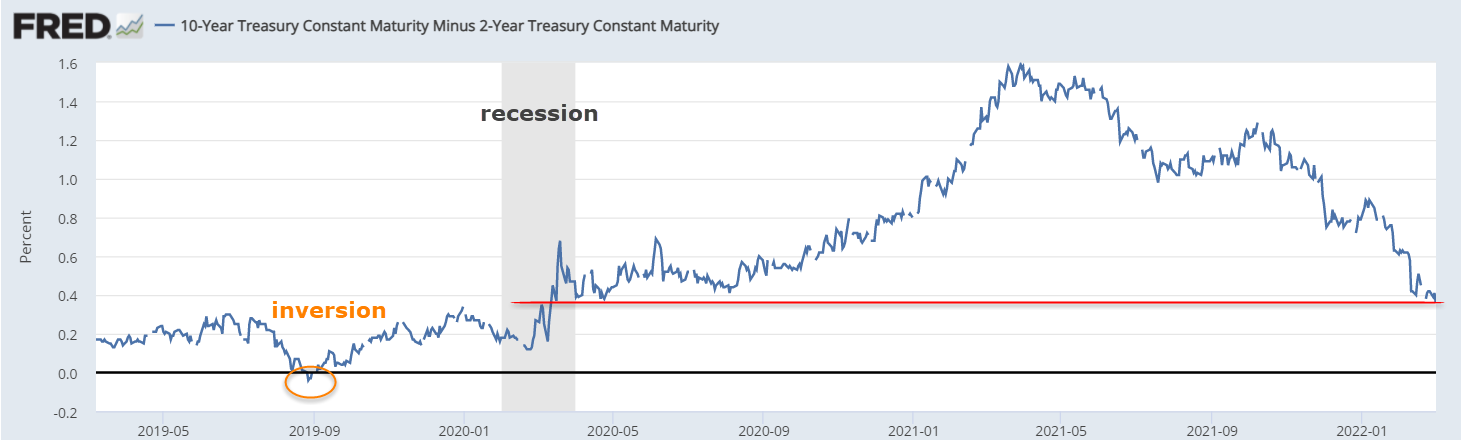

Again, context in multiple timeframes is important. On that note, the 2s-10’s spread (that has forecast every U.S. recession since WWII) flattened the most since the March 2020 COVID crash, which is the market moving to price in a recession, likely the result of the Fed’s policy path to neutralize inflation and now geopolitical tensions. As I’ve long said, the Fed would rather an economic recession than a hyper-inflationary event and there’s no doubt that the Biden administration feels the same.

2’s-10’s spread flattening

2’s-10’s spread flattening

HYG (+0.25%) wasa bit weaker today than the last several days on a relative basis, but that’s to be expected with the massive jump in yields.

SP-500 (1m) and HYG

SP-500 (1m) and HYG

My broader credit index still looks quite good considering…

SP-500 (2m) and my credit index

SP-500 (2m) and my credit index

Currencies and Commodities

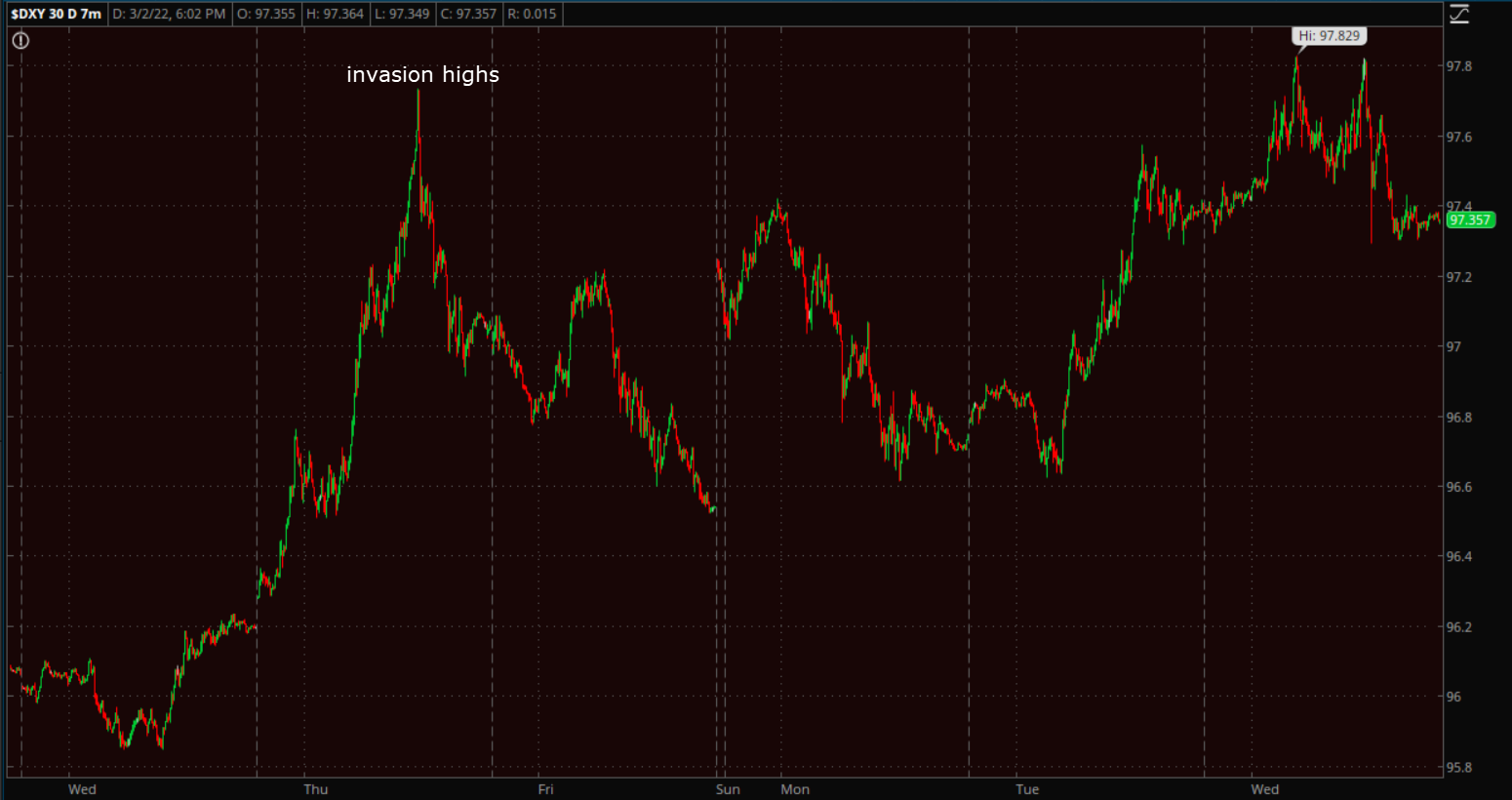

The U.S. Dollar Index dipped today as Powell spoke (dovish signal relative to expectations) and after testing last week’s flight to safety invasion highs. The U.S. Dollar Index dipped -0.1% to 97.34.

U.S. Dollar Index (1m) with a modestly positive/dovish reaction to Powell

U.S. Dollar Index (1m) with a modestly positive/dovish reaction to Powell

U.S. Dollar Index (7m) testing last week’s flight to safety highs before pulling back.

U.S. Dollar Index (7m) testing last week’s flight to safety highs before pulling back.

The Australian Dollar was already in a modestly supportive position relative to the benchmark index coming into the week.

AUD/USD (daily) trading above the risk-on/risk-off line in the sand at the H&S neckline around 0.72.

AUD/USD (daily) trading above the risk-on/risk-off line in the sand at the H&S neckline around 0.72.

Notice the Aussie’s (2m) positive change in tone in today’s cash session, ending the day with a bullish consolidation which bodes well for a modestly positive risk environment.

Notice the Aussie’s (2m) positive change in tone in today’s cash session, ending the day with a bullish consolidation which bodes well for a modestly positive risk environment.

Crude prices soared even higher with WTI topping $112. WTI crude futures settled sharply higher by +7.4% to $111.04/bbl. The spike in oil prices was attributed to increased expectations for supply constraints after Russia continued its offensive in Ukraine, and OPEC+ left supply increases as expected at 400k bbl per day.

For context of the last 2 days’ gains, here’s the daily chart…

WTI Crude (daily) – this is a major conundrum for the Fed. On one hand they could be forced to inject liquidity to make up for Russian liquidity due to sanctions – although Powell suggested there’s plenty of liquidity in the plumbing of the global financial system earlier today (although S&P futures may argue otherwise, but the Fed is more concerned with Dollar liquidity), and that would exacerbate inflationary pressures, but at the same time Crude has been soaring exacerbating inflationary pressures in the global energy market. Unintended and unforeseen consequences are seemingly limiting the Fed’s options.

WTI Crude (daily) – this is a major conundrum for the Fed. On one hand they could be forced to inject liquidity to make up for Russian liquidity due to sanctions – although Powell suggested there’s plenty of liquidity in the plumbing of the global financial system earlier today (although S&P futures may argue otherwise, but the Fed is more concerned with Dollar liquidity), and that would exacerbate inflationary pressures, but at the same time Crude has been soaring exacerbating inflationary pressures in the global energy market. Unintended and unforeseen consequences are seemingly limiting the Fed’s options.

Gold futures pulled back today lower by -1.1% to $1,922.30/oz as headlines suggested another round of talks between Russia and Ukraine was coming on Thursday.

Gold futures (1m)

Gold futures (1m)

Overall, however, gold still looks like it may be in a larger, more volatile symmetrical triangle consolidation and 3C charts are still supportive.

Gold futures (30m).

Gold futures (30m).

For more on gold’s outlook, see this morning’s Early Update...

“As long as Gold futures don’t trade below $1892 (make a lower low), then the potential bullish symmetrical triangle (I say potential because it’s bigger, easier and more volatile than a typical triangle consolidation), can remain intact with a second leg upside target of $2045.”

Bitcoin (currently -1.1% for the day) saw a modest decline as expected as it ran into resistance yesterday around $45k.

BTC/USD (daily). For more, here’s an excerpt from this morning’s Early Update…

BTC/USD (daily). For more, here’s an excerpt from this morning’s Early Update…

” There are a few constructive developments like an aborted bear flag and an emerging price trend of higher lows (blue circles), although this would not be considered a bullish consolidation because of the preceding trend (down), a bullish consolidation is a break or breather within an uptrend. This may be a transitional area. Bitcoin needs a clean breakout on heavy volume above $46k to really start to change the picture to a more bullish one.”

Despite the pull back from resistance (nothing wrong with that), when looking at BTC as a barometer of risk sentiment in a speculative asset class, it’s still positive vs. S&P futures…

S&P futures vs. Bitcoin futures (15 min.)

Summary

The CNN Fear and Greed Index (25) is higher than yesterday (18), but still in extreme fear and extremes in sentiment tend to be contrarian signals.

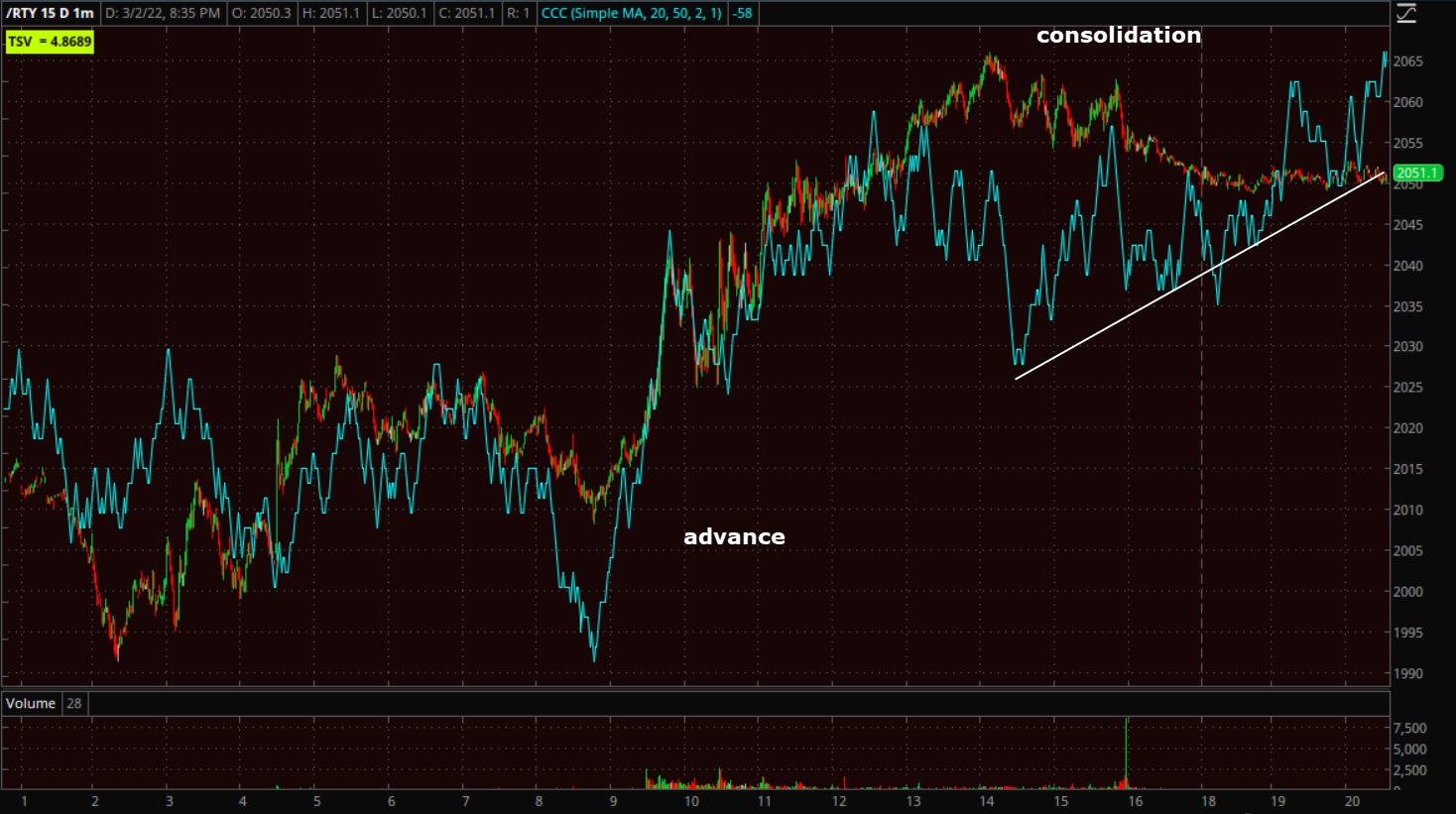

The development and subsequent breakout of bull flags is an obvious positive. Ideally for the bullish case volume would have increased, but that’s not unusual and not a deal breaker. The market is 1-day overbought and it would be helpful for the entire measured move (about another +4% for the S&P) to work off those overbought conditions in a small consolidation and there’s some evidence to point to that this afternoon.

IWM (5m) While having long exposure to the market it would be exciting and nice to see price make a vertical leap higher, in all practicality I’d prefer a small consolidation (such as we see this afternoon in blue) to work off the dangers of an extremely overbought market and allow the trend to continue without major price volatility in in response to overbought conditions. I always prefer a strong trend with consolidation to work off overbought/oversold rather than parabolic spikes which have a strong tendency to be unpredictable , prone to sharp and sudden reversals.

IWM (5m) While having long exposure to the market it would be exciting and nice to see price make a vertical leap higher, in all practicality I’d prefer a small consolidation (such as we see this afternoon in blue) to work off the dangers of an extremely overbought market and allow the trend to continue without major price volatility in in response to overbought conditions. I always prefer a strong trend with consolidation to work off overbought/oversold rather than parabolic spikes which have a strong tendency to be unpredictable , prone to sharp and sudden reversals.

While my sense is that the Russia/Ukraine war will not turn in to a major global economic event in terms of growth, it does seem there’s a high risk of it exacerbating inflation as we already see in Energy prices. To make matters worse, the sanctions have a probability of affecting liquidity and the last thing the Fed wants when trying to shrink their balance sheet to fight inflation, is to suddenly have to expand it in liquidity operations, so in that sense, the war is a major risk that ultimately could hamper the Fed’s already questionable ability to skillfully handle inflation. said another way, the war may not be the major negative event that many have feared, but the little seen, unforeseen consequences could be quite damaging in ways most didn’t imagine. 2022 is definitely getting off to a much rougher start than 2021, and to think the market was whistling past the graveyard right up until the first trading day of the new year.

It goes without saying that a lot will depend on cease-fire talks scheduled for tomorrow. Despite today’s strong performance at the index level, there’s still some clear trepidation evident in many areas. Off the top of my head the fact we didn’t see more short covering today suggests traders are conditioned to the daily flip flop regarding Russia/Ukraine, but a second day of follow through gains may just do the trick and force them to buy to cover.

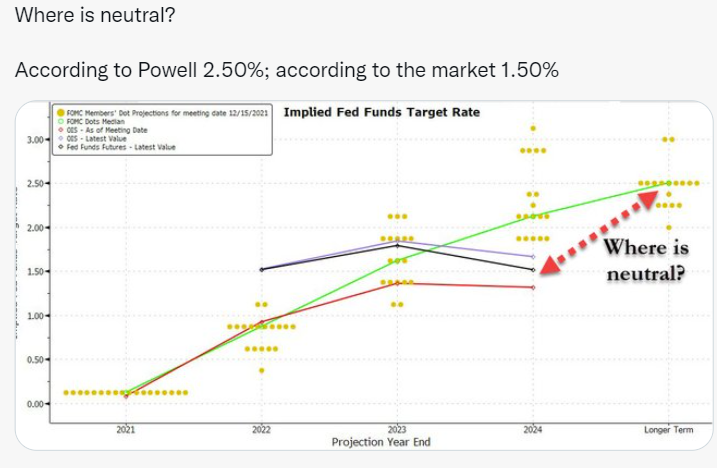

with regard to Powell today, I’m not sure how much the market picked up on the comment,

“WE TALK ABOUT GETTING TO NEUTRAL RATE OF 2% TO 2.5%, AND IT MAY NEED TO GO HIGHER THAN THAT”

The market has been pricing ina neutral rate more along the lines of 1.5%. As a quick reminder, it was almost this exact scenario in early October of 2018 that sparked a 20% decline in the S&P that started a day after Powell said that he wasn’t sure where the neutral rate was (as the Fed was in the midst of a rate hiking cycle), but he felt it was higher.

As of tonight, I see no strong reason to doubt the full second leg measured move which on the conservative side would be another 4% or so higher for the S&P.

Overnight

S&P futures are down -0.2% tonight, very much along the lines of the pause/consolidation seen on IWM’s price chart this afternoon. 3C looks constructive during this small consolidation phase.

Russell 2000 futures (1m)

Russell 2000 futures (1m)

VIX futures are not showing the same afternoon nervousness as VXX, they actually look a bit weaker on 3C charts which helps to confirm the price consolidation in index futures.

The U.S. Dollar index is up +0.1%

WTI Crude is up +2.5% to $113.40 (inflationary).

Gold futures are up +0.45%, but this looks like a bearish consolidation of the day’s losses. See comments on gold above and from earlier today.

Bitcoin futures are near flat (+0.2%).

Treasury futures are seeing a modest bounce/consolidation, which like index futures, is not surprising after the day’s losses. The 2-yrear yield is down 4 bp and 10-year yield down 2 bp. both are consentient with a correction and don’t raise any alarm bells for me that there’s some inside information on tomorrow’s negotiations suggesting this is the start of another flight to safety.